HVACR sales in EMEA market 2013

29th September 2014The latest Eurovent Market Intelligence sales figures for HVACR equipment in 2013 reflect a generally depressed market but future prospects are encouraging.

Fan coil units

The fan coil unit market in the EMEA region registered sales of some 1.45 million units, similar to 2012. European sales continue to represent approximately 75% of the market.

The fan coil unit market in the EMEA region registered sales of some 1.45 million units, similar to 2012. European sales continue to represent approximately 75% of the market.

Despite a contraction of about 10% compared to 2012, Italy is still the major market with 25% of all sales, followed by France with a 14% market share. Sales in Germany and the UK remained modest, each with a market share of approximately 5%. Spain and Portugal which recorded respective rises of 8% and 3%. However, the tides have turned for Poland and the Northern countries, which have dropped by 10% and Russia which experienced a sharp 4% decline after two years of growth.

Outside of the EU, Turkey stands out with its continued steady growth and a market share close to 10% this year against 7% the previous year. Russia is behind it with 7% of sales in the EMEA region. Sales in the Middle East in 2013 were approximately 260,000 units in 2013.

This year fan coils are expected to achieve the same level as 2013 with perhaps some slight growth of around 1.5%. The forecasts remain positive for already dynamic areas like Russia and Spain. However, prospects for Italy are more gloomy which began the year with falls varying from -3 to -10%.

The 2-pipe fan coil still commands 75% of the market except in Turkey and the Benelux countries where the ratios are the same. In terms of design types, cased fan coils and uncased models each represent 30% of the market. The remaining market is split in equal parts between cassette-type models and ducted models.

Rooftops

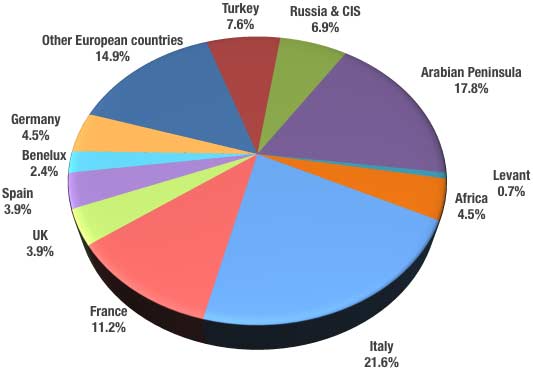

The rooftops market in the EMEA region amounted to around 60,000 units in 2013 – 5% up on 2012. The Middle East still leads the way with more than 80% of the market, then Africa coming in a distant second with 4.2% of the market.

Within Europe, the market distribution is more even. Ahead of the pack are France and Spain with market shares nearing 20%. Then come Turkey, the UK and Italy with approximately 10% each. The rooftops market remains a dynamic market unlike others, with considerable 2012-2013 growth and upward 2014 forecasts. Contrary to previous years, Europe had the highest growth rates with the UK showing a 30% increase. Spain and Turkey saw increases of up to 20% with France increasing but more subdued with a 4% increase. A serious setback in Italy saw a drop of approximately 15% this year.

In general, medium-capacity units of 17-72 kW are the most popular rooftop unit-types accounting for around two-thirds of total sales. Small-capacity units of under 30kW are on the rise in the Middle East, but it is the units of over 30kW, which easily easily account for most sales in the rest of the EMEA region.

Chillers

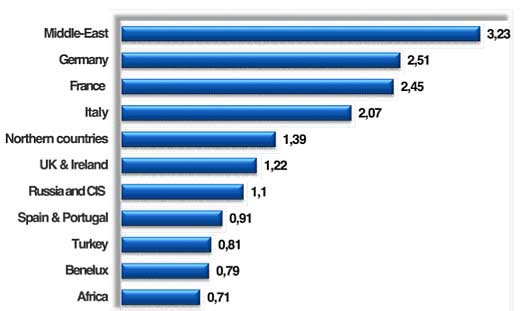

The chiller market continues to grow, reaching 20 millions of kW in 2013 against 17 million in 2012. The largest market is the Middle East with 18% followed by Germany (15%), France (14%) and Italy (12%).

The chiller market continues to grow, reaching 20 millions of kW in 2013 against 17 million in 2012. The largest market is the Middle East with 18% followed by Germany (15%), France (14%) and Italy (12%).

In the small-capacity category of under 50kW, the majority of sales were concentrated in the South of Europe. Italy commands a market share reaching 45% and is followed by France with 13% and the Iberian Peninsula with 6%. Germany has a respectable market share nearing 9%.

For medium-power machines, the market was again led by Italy, France and Germany with respective market shares of 16%, 14% and 10%. The Benelux countries, Nordic countries, UK and Spain which fluctuate around 6%.

The Middle East dominates the market for high-capacity (above 700kW) machines with 25% of the market. Coming in second position, are Turkey and Russia with 8% of the market and then the usual trio of France/Germany/Italy with respective market shares ranging from 6 to 7.5%.

Compared to 2012, there has been a market stagnation for machines of over 50kW in the EMEA region. By contrast, Scandinavia and Turkey, with 14% and 8% increase respectively, eclipsed the negative trends in other countries.

Overall, looking at the 28-member European Union, the year has been less than buoyant. The fall has been most significant in the UK and Ireland with a 9% drop, followed by France, down by 6%. In the Iberian peninsula, in Germany and in Italy small contractions in the market were reported ranging from -3% to -0.5%. Chillers sales were also down in Africa, primarily due to South Africa, which recorded a 20% fall between 2012 and 2013.

Over three-quarters of chillers sold in the EMEA region are air-cooled. Only 10% of sales are for water-cooled units. R410A is the major refrigerant, being found in 80% of all units. R134A comes next with 14%.

Computer room air conditioners (CRAC)

Of the approximately 30,000 units sold in EMEA in 2013, over 25,000 units were sold in Europe. The market leader remains Germany with 12.5% of the market share followed very closely behind by the UK with 11%. Russia and its ex-satellites continue to hold third place on the market with 10.5%, with 3,200 units sold. The Middle East and Africa have respective shares of 9.5% and 6.5%.

Of the approximately 30,000 units sold in EMEA in 2013, over 25,000 units were sold in Europe. The market leader remains Germany with 12.5% of the market share followed very closely behind by the UK with 11%. Russia and its ex-satellites continue to hold third place on the market with 10.5%, with 3,200 units sold. The Middle East and Africa have respective shares of 9.5% and 6.5%.

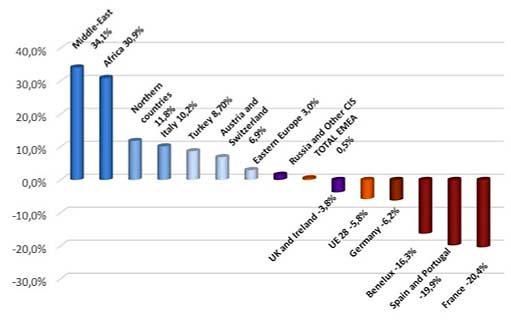

The CRAC market in EMEA had a weak year in 2013, almost stagnating at around 0.5%. Within the EU, the market declined sharply (down 6%) with drops of up to 20%. France, the Benelux countries and Spain suffered the most with drops ranging from 16% to 20%. Germany was also affected with a contraction in the region of 6%, the same goes for the UK and Ireland with a 4% drop. Only Italy and the Scandinavian countries saw their market shares grow by 10%. The EMEA region, the Middle East and Africa record the highest increases at 30%, followed by Turkey and the Austria/Switzerland duo 8% up and Eastern Europe up 3%.

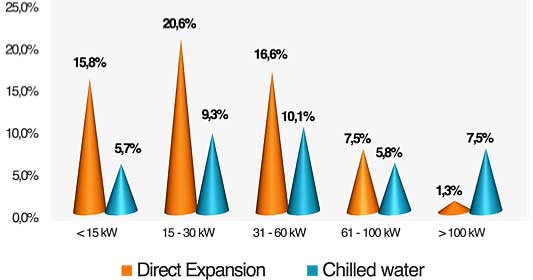

Two-thirds of the units sold in the EMEA region are direct expansion units and the remaining third are chillers. Amongst the chillers, the medium-capacity machines (between 15 and 60kW) represent half of all sales. The distribution is reported to be more even for direct expansion machines as sales include almost as many small-capacity (under 15kW) as medium-capacity machines.

Two-thirds of the units sold in the EMEA region are direct expansion units and the remaining third are chillers. Amongst the chillers, the medium-capacity machines (between 15 and 60kW) represent half of all sales. The distribution is reported to be more even for direct expansion machines as sales include almost as many small-capacity (under 15kW) as medium-capacity machines.

Air handling units

This year once again, the air handling unit market is said to have fared relatively well, with a rise of 2.8% in 2012-2013 in the European Union, and an increase of over 10% in the Middle East. The main driver behind this rise is reported to be Germany, which totals nearly 20% of all sales in the EMEA region with a market share estimated at €356m in 2013, and an annual growth rate of +10%. Scandinavia, the other heavyweight in the region, with its 15% market share, saw its sales stagnate in 2013 compared to 2012. Substantial progress was made by Russia and Turkey, which respectively recorded increases of 17% and 46% respectively. Between them they commanded over 13% of the market in 2013. To a lesser extent, Spain and the Czech Republic saw an increase of 8%, respectively reaching €40.1m and €21.2m in 2013. France saw its market share rise by 4% to approximately €112m in 2013.

This year once again, the air handling unit market is said to have fared relatively well, with a rise of 2.8% in 2012-2013 in the European Union, and an increase of over 10% in the Middle East. The main driver behind this rise is reported to be Germany, which totals nearly 20% of all sales in the EMEA region with a market share estimated at €356m in 2013, and an annual growth rate of +10%. Scandinavia, the other heavyweight in the region, with its 15% market share, saw its sales stagnate in 2013 compared to 2012. Substantial progress was made by Russia and Turkey, which respectively recorded increases of 17% and 46% respectively. Between them they commanded over 13% of the market in 2013. To a lesser extent, Spain and the Czech Republic saw an increase of 8%, respectively reaching €40.1m and €21.2m in 2013. France saw its market share rise by 4% to approximately €112m in 2013.

Italy underwent a small market contraction, seeing sales drop by 2.6%, and particularly Portugal which dropped 20% to €6.1m.

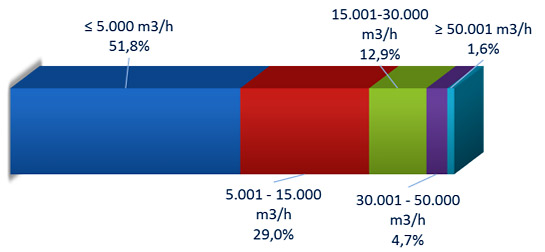

Units of under 5,000m3/hr continue to be the most popular, commanding 52% of the market against only 6.3% for units of over 30,000 m3/hr.

The European market is forecasted to experience a small contraction this year after the first two quarters showed consecutive falls of 2% and 3%. At the same time, there is a contraction in the number of market players, with a few small ones disappearing or being taken over by larger ones.

Air filters

The air filters market was quite depressed in 2013 with a contraction of 0.7% in the EU and almost stagnating at -0.4% for the rest of the EMEA region, stabilising at around €1.08bn. This lower growth rate may be explained by an extension of the lifetime of the filters in place or the increasing importance of external supplies, such as China or India. Germany, the biggest market with €208m of sales in 2013, grew moderately by about 4%, while France, the second largest market, saw its market stagnate at around €121m. The Scandinavian countries, which represent between the four of them approximately 15% of the EMEA region, saw their market decrease by about 5%, as did Switzerland. Italy and Spain saw their sales increase by 6% for the first quarter and over 15% for the second.

The air filters market was quite depressed in 2013 with a contraction of 0.7% in the EU and almost stagnating at -0.4% for the rest of the EMEA region, stabilising at around €1.08bn. This lower growth rate may be explained by an extension of the lifetime of the filters in place or the increasing importance of external supplies, such as China or India. Germany, the biggest market with €208m of sales in 2013, grew moderately by about 4%, while France, the second largest market, saw its market stagnate at around €121m. The Scandinavian countries, which represent between the four of them approximately 15% of the EMEA region, saw their market decrease by about 5%, as did Switzerland. Italy and Spain saw their sales increase by 6% for the first quarter and over 15% for the second.

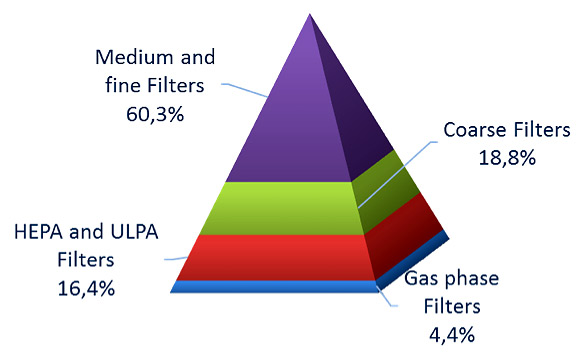

The market share of fine and medium filters has continued to increase these last few years, achieving 60% of the market in 2013. Next in line are the coarse filters with 19%, and then the HEPA-ULPA filters with 16%. Gas-phase filters barely represent 5% of sales.

Cooling towers

The cooling towers market experienced a contraction of around 7% in the EMEA region, falling to €229.5m in 2013, that is a level even lower than that of 2011. Topping the sales charts is still Germany with over €38.4m, followed by Russia and its ex-satellites, which have almost €23.4m.

Italy, France and the UK are still the main secondary players with 8% of the market each.

Those exhibiting greatest growth were Russia, up 23%, along with Poland which achieved €8.2m in 2013 with an increase of over 30%. Conversely, those with the largest declines were France and the UK brushing the -20% mark. In the EMEA market in 2013, much more open than closed cooling towers were sold in a ratio nearing 65/35.

Heat exchangers

The heat exchangers market increased to €809m in 2013 in the EMEA region, which is approximately 15% more than in 2012. Aside from Germany with its 17% market share, the main players are Russia and Italy with 10%, France and the UK with 8% and the Middle East with 7%. Leading the way with highest growth are the Benelux countries, Russia, the Middle East and the Scandinavian countries, recording rises over 20%. Conversely, Italy experienced a small contraction in its market share, while Germany and the UK saw some growth of around 5%.

Adiabatic coolers

For some years now, has increasingly reported the comeback of a technology as old as the hills – that of adiabatic coolers. It is a backup system used temporarily when the summers become too hot, and this is why this technology is still barely used in the North of Europe and is absent in the Middle East. Its main markets are currently in countries with temperate climates like Germany, France, Switzerland and Eastern Europe.