Rooftop sales grow by 10%

19th July 2017EUROPE: The market for rooftop units grew by almost 10% last year, according to latest figures for Europe, the Middle East and Africa from Eurovent Market Intelligence.

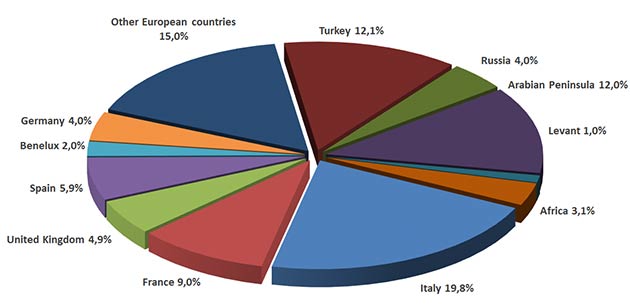

The European rooftop unit market grew to around around 12,900 units in Europe last year. The biggest market was Turkey, with the 2,500 units sold representing a growth of around 12%. Italy and Spain saw growth rates of 20% and 4% respectively, and unit totals of 1,690 and 1,800. France saw sales drop by 12% but was second in market size behind Turkey with 2,350 units sold.

Medium-capacity units between 17kW and 120kW were the biggest sellers in Europe, with reversible units the most common and accounting for around 65% of the market. Around 64% were for new build.

Fan coils

After good growth in 2015, the fan coil market stabilised in 2016 at 1.61 million units (up 3%) in the whole EMEA zone. Good sales growth was experienced in Turkey and Russia, with increases of 40% and 15% respectively. The markets in Spain and the UK continued to grow (20% and 7% increases, respectively) and remained relatively stable in countries like France and Germany. In Italy, however, which accounts for almost 20% of the fan-coil market in the EMEA zone, sales fell by 4% and were at around 318,000 units in 2016.

Two-pipe units still account for around 77% of the market as opposed to 23% for 4-pipe units. From the point of view of design, fan coils with and without horizontal bodywork account for 30% each of the market while cassette and ducted units account for the rest of the market.

Air handling units

The air handling market in Europe in 2016 was up to €1.9bn, €409m of which was in Germany, €321m in Northern Europe, €220m in Eastern Europe, €130m in Turkey and €131m in Russia and the CIS. As in 2015, the market remained stable within the EU. In contrast, the market fell in Russia and the Middle East, with decreases of around 20%. In Africa the market lost 15% of its value. There had been a sharp fall in Germany in 2015, but the figures stabilised last year. Germany remains the largest market, accounting for almost 20% of the turnover, followed by the Nordic countries at almost 15%.

The European market numbers are led by low power units below 5,000m³/h, accounting for around 60% of units sold, of which 16% were below 1,000m³/h). In the Eurovent energy classification, over half are in the highest categories (A and A+) and 15% in category B.

Within the European Union, the type of exchanger is divided almost 50/50 between plate and wheel exchangers, compared to just 5% for run-around-coil and heat pipe exchangers. Almost 40% of the units sold are compact.

Chillers

The chiller market reached 24.5 million kW in the EMEA zone in 2016, 16.5 million of which was in the EU.

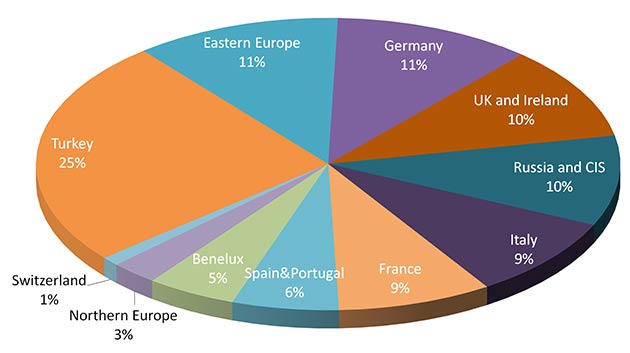

In Europe, Eurovent Market Intelligence sees a clear segmentation among the different powers. Small and medium-power units are sold mostly in the south of Europe. As in previous years, Italy, France and Spain have a preference for machines under 700kW. Italy kept its position as market leader with a share of 25%. France and Spain came next with market shares of around 12%. For machines over 700kW Turkey is leader with a market share of 15%, closely followed by Germany at 13.5%.

France and the UK both saw sales drop, by 12% and 20% respectively. The markets in Spain, Italy and Germany were more stable but in Russia the market fell by 10%.

IT cooling

The market for IT cooling was up to 29,300 units sold within the EU in 2016, of which 65% were CRAC, 18% row and rack coolers, 16% TLC mobiles and 1% air handling units. Italy leads the way with 5,300 units sold, followed by Germany at 4,630 units and then France and the UK at roughly 3,800 units each.

The market for computer room air conditioners fell by 10% in the EU. In Spain and Portugal the fall was 12%, while the sharpest fall came in Italy at 24%. By way of contrast, Benelux and France were in good health, with growth rates of 8% and 6% respectively.

In the EMEA zone, two-thirds of the units sold are direct expansion while the others are chillers. This proportion is said to be the same for numerous countries in the area except France and Germany, where more chillers are sold, accounting for just over 50% of sales. As regards power, 50% of the chillers sold are over 60kW while 60% of the direct expansion units are under 30kW. There also appears to be an upward trend in CRAC units with a modulating compressor (14% of units sold) and the free-cooling option (4%). On the TLC market, free-cooling already accounts for half of the units sold.

Air filters

As in previous years, the filter market remained stable in the EU at almost €950m. Germany remains leader with a market share of 19%, followed by the Scandinavian countries at 14% and close behind, France at 12%.

As far as growth is concerned, Sweden and France stand out with high growth rates of 20% and 12%. Germany, the UK and Denmark shrank by around 2%. The situation in Russia, Africa and the Middle East, however, is decidedly gloomy, with falls of over 10%.

Heat exchangers

After a slight fall in 2015, the heat exchanger market stabilised in 2016 with a total of €990m in the EMEA zone. This stability is due to France and Spain, while the market in Italy and Germany fell by 6%.

In terms of market share, Germany had the largest share at 15%, followed by Italy at 11% and then France at 9%.

Outside the EU, Russia had the largest market share at 10%, followed by the Middle East at 9%.

Contrary to previous years, air-cooled exchangers gained market share and in 2016 accounted for 25% of the market. The rest of the market consists of evaporators (45%), condensers (22%) and CO2 and air exchangers (8%).

As for application, the market is still dominated by commercial (29%) and industrial (19%) refrigeration, with just 17% used for comfort (central heating, air conditioning, etc); machine renewal accounts for 66% of the market in the EMEA zone, compared to 34% for new build projects.

Cooling towers

The cooling tower market shrank by around 5% in 2016 in the EMEA zone. France, Germany and Spain experienced falls of up to 20%, while the situation improved in other countries such as the UK and Turkey, with growth rates of around 12%.

The market leader in Europe is Germany at 11%, followed by Italy (9%) and close behind, Turkey (8%). Outside Europe, the Middle East has a market share of 12%.

The technology of cooling towers remained unchanged in Europe: open towers still account for almost two-thirds of the market in comparison to closed towers. In some countries, such as Belgium, it is the other way round, while in France and Turkey closed towers sell slightly more than open ones. As for the power installed, most installations (60%) are under 10 cells, while only 2% are over 50 cells. Larger powers are found mainly in Russia and its ex- satellite countries (CIS), and also in Finland and Turkey.

Chilled beams

The chilled beam market was up to €65m in Europe in 2016, €28m of which was in Northern Europe (the largest market), around €6m in France, €3.2m in Italy and €2.8m in Germany. The European market grew by 10% as a whole. This was mainly due to impressive growth of over 20% in Sweden, Italy, the UK and Ireland. Good growth was also seen in Eastern Europe at around 15%. The Russian market fell, however, by over 20% and the French and Turkish markets were down 5%.